FEBRUARY 2024

One of our most consistent fund picks: Schroder ISF Asian Total Return Fund

My relationship with this fund goes back to its launch in 2007, when I purchased a holding and have subsequently added it to buy lists as my modest career progressed through different houses. It has remained on CAM’s BUY list, with the agreement of my colleagues’ since not long after I joined in 2009. So, I can safely say that I know the fund and its management team well. The performance since launch justifies my decision to invest, with the chart below showing the fund versus its peer group and relevant benchmark.

As you would expect, the CAM Research team monitor our investment decisions to help improve our efficiency. The longer the track record, the more confidence we have in the data. In this instance the Schroder ISF Asia Total Return Funds has been one of our best and most consistent fund picks versus its own index and peer group. Absolute performance has also been very attractive.

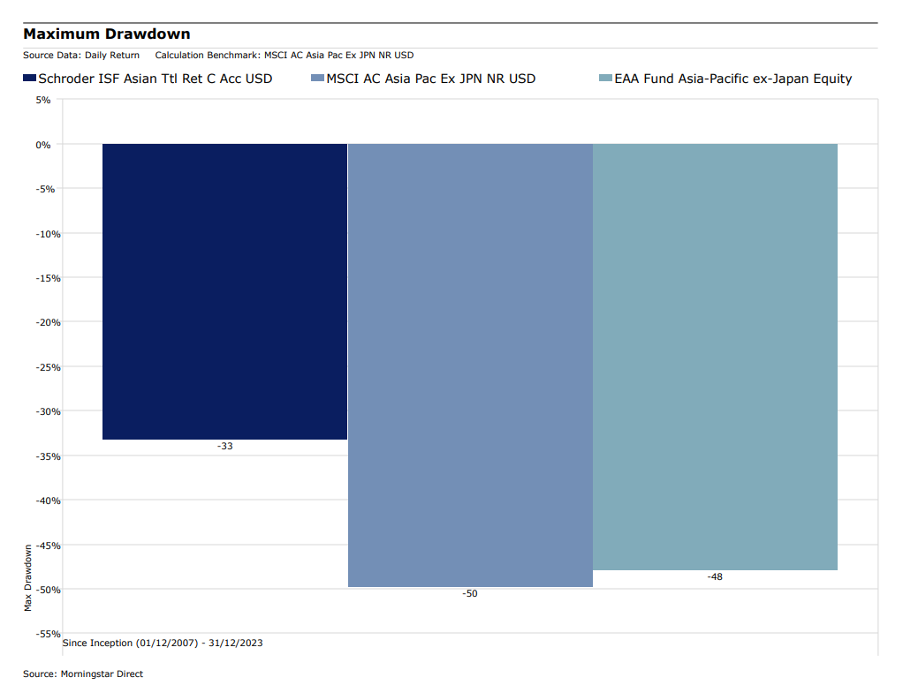

The management team, of Robin Parbrook and King Fuei Lee, follow an active approach (they do not make decisions based on aiming to replicate the benchmark but invest in holdings that they believe to be attractive based on Schroders’ considerable Asian presence.) The team also make use of the rules that govern open ended collective investment schemes, allowing for a judicious use of hedging. The team seek to add in protection to the holdings by entering into contracts that will pay out if the value of the index as a whole falls, not the individual names that they hold. This ‘short’ position versus the index gives downside protection; it aids in defending the value of the fund when, as they do, markets prove challenged over the shorter term. In other words, the managers reduce market exposure to help protect assets. Being candid all investments run the risk of drawdown over the near term or short periods. Investing in Asia is no different, in fact many consider it a higher risk asset within equities. The fund’s management team realise this and as mentioned use a hedging strategy to limit drawdowns. The outcome of this can be seen below versus the benchmark. Losing less in a challenged environment means the starting point for a rebound is higher.

Costs and charges is an issue that has always played a role within our assessment but can prove emotional. A very simple ‘expensive is bad’ and ‘cheap is good’, in my view, does our clients a great disservice. In our diversified portfolios we have a mix of what one would consider very cheap, with some expensive holdings. They all have a role to play. In this instance the fund is at the higher end of the range of what cost I am prepared to pay. How do I justify this and explain to the layperson? The best analogy I can use is shoes. Have a look at your own collection, most likely a mix between cheap and expensive. This fund falls into the Church’s or Jimmy Choo, depending on your preference. If one casts an eye back to the first chart indicating performance, I argue it is cheap for what unitholders receive. The Overall Cost of Funding (OCF) is 1.3% which includes all charges, remember the chart displays the actual return a unitholder received, it is net of all fees. A tracker fund’s OCF will pale in comparison to this, but so does the performance.

As this fund is actively managed, the management team pays scant attention to the benchmark; whilst the managers know it exists and they are measured against it, the construction of the index plays no part in the portfolio’s active approach. If I am going to pay up for an actively managed fund, I want it actively managed. The industry suffers from charlatans; there are too many funds purporting to be actively managed when in fact they are closet trackers but charge a full fat management fee. The following chart displays the fund and peer group at country level when compared to the benchmark. This fund not only differs when compared with the benchmark but also the peer group.

Since launch in November 2007, the fund has consistently outperformed its benchmark and the peer group. Using a beneficial combination of quantitative and qualitative investment assessment, the fund leverages Schroder’s substantial presence and investment skill within Asia. This is why it is used as core Asia equity exposure within our clients’ portfolios. Expensive, maybe, but definitely worth it.

This commentary was prepared by James Calder.

James joined City Asset Management in 2009 and is our Chief Investment Officer, where he is responsible for managing the investment process and chairing the asset allocation, portfolio construction and fund selection committees. He is also a board member. He has 25 years’ experience, including roles at Gartmore, BestInvest and Baring Asset Management, and specialises in multi-asset real return investing. Throughout his career he has been a key mentor for younger analysts and enjoys watching them progress on to their own successful careers. In his spare time, James enjoys clay pigeon shooting, mountain biking and spending time with his family.