Time for an Inheritance Tax Rethink

Estate planning is something many of us put off for understandable reasons. However, procrastination has become an expensive option following the changes to inheritance tax (IHT) introduced by the Chancellor in her last two Budgets.

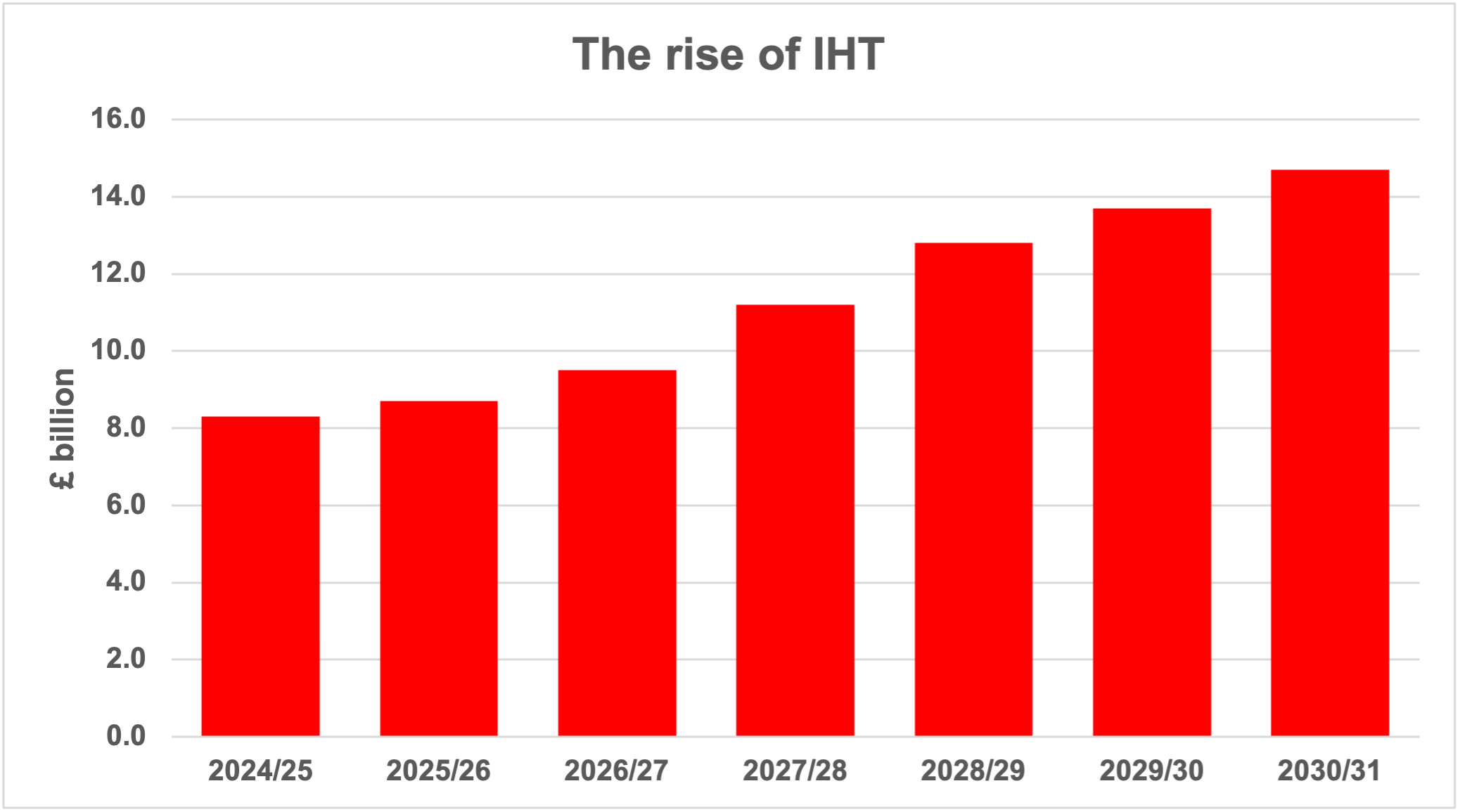

Source: OBR EFO March 2026

The changes

The Chancellor has introduced two major reforms which will see the amount of IHT raised increase by nearly 70% between 2025/26 and 2030/31:

Business and agricultural reliefs. New IHT reliefs for businesses and farms came into effect on 6 April after considerable controversy. The most significant was the creation of a £2.5 million capped allowance on the amount of business and/or agricultural property which can qualify for 100% IHT relief. The allowance is transferable between spouses and civil partners in the same way as the IHT nil rate band. Once the allowance is exceeded, relief is reduced to 50%.

There has also been a reduction in IHT business relief for holdings of eligible AIM shares, which is now 50% in all instances.

Pension death benefits. From 6 April 2027, most pension death benefits (other than death-in-service) will be treated as part of the deceased’s estate and potentially subject to IHT. As income tax also generally applies to pension death benefits on death at age 75 or older, this can mean that the overall tax rate on an unused pension fund is as much as 67% (68.8% in Scotland).

There was one other IHT Budget change which arguably counts as continued no change. The nil rate band (£325,000 since 2009) and residence nil rate band (£175,000 since 2020) are now frozen until 5 April 2031.

Rethink

The reforms are already prompting some of those affected to rethink their estate planning strategies. Building up a large pension pot to pass over on death is no longer the cunning plan it once was. Similarly, waiting to transfer a business or farm until the will is read may now make less sense than a lifetime gift.

If the new regime makes an IHT bill inevitable, this could be the time to revisit an old solution to IHT – whole of life assurance placed in trust for your beneficiaries to help fund the tax liability whenever it arrives.

Action

IHT is a rapidly increasing source of tax revenue that could see HMRC as one of the larger – if the not the single largest – beneficiary of your estate.

If you have not reviewed your estate planning in 2026, now is the time to do so.

This article was prepared by Chris Green, our Head of Financial Planning. We always appreciate your feedback. If you have enjoyed this article or have any specific topics you would like to see addressed in future newsletters, please email us at FPTeam@city-asset.co.uk.