Tax Distortions and Disincentives

When the Office for Budget Responsibility (OBR) and the Organisation for Economic Cooperation and Development (OECD) both highlight distortions in the UK tax system, this suggests there are serious problems. The OBR is sufficiently concerned that it has promised to “conduct further analysis of UK marginal tax rates relative to other countries” in its 2026 Fiscal Risks and Sustainability Report. For its part, the OECD recommends that the UK “conduct an in-depth tax review to make the tax system more efficient and growth-friendly by reducing distortions, closing loopholes, and ending reliefs and exemptions that do not serve economic or social objectives”.

The OBR and OECD agree…

“…a higher level of the tax take increases the risk that incentives within the tax system distort or constrain economic activity by more than expected. While the level of the tax take in the UK is not unusually high compared to other advanced economies, there is some evidence that UK marginal rates of tax may be above the OECD average and this may be more relevant for impacts on incentives to work, save, and invest.”

OBR Economic and Fiscal Outlook March 2026

“There is scope to improve the efficiency and fairness of the UK tax system. Parts of the tax system are complex, leading to large compliance costs... Furthermore, distortions such as kinks in the income tax schedule weaken work incentives…”

OECD April 2026

The income tax rollercoaster

One target of the OBR and OECD is the way in which successive UK Chancellors have tweaked the income tax rules to raise more revenue without touching the political third rail of headline tax rates. The Chancellors’ focus has been on meeting short-term fiscal targets with seemingly little or no thought given to the broader consequences for the economy. To make matters worse, many of the income tax allowances and thresholds have been frozen for years, with some, such as the personal allowance and higher rate threshold, not due a thaw until at least 6 April 2031. That means, each year, a new group of taxpayers encounters the tax distortions as their income rises.

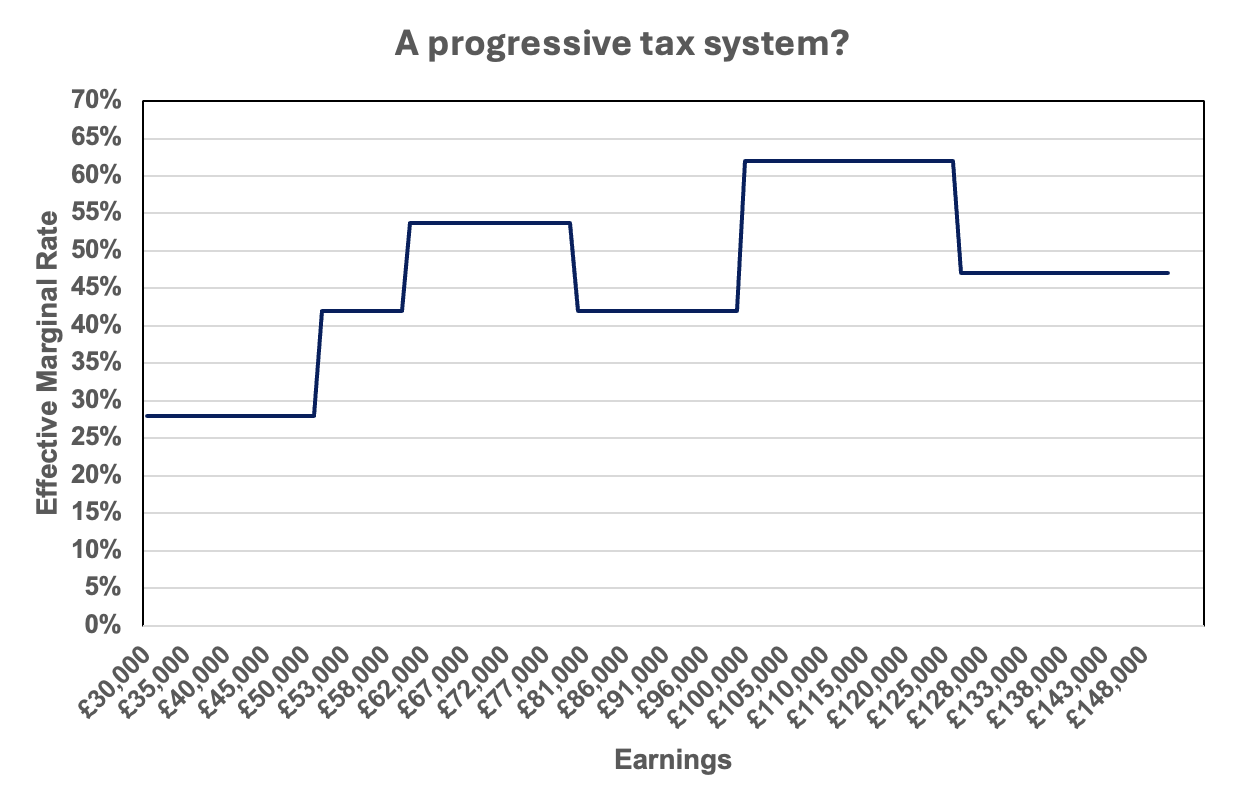

The graph below is a simple example of how the UK income tax system (outside Scotland), creates a roller coaster of tax rates for an employee with two children eligible for child benefit:

Based on an employee with two children aged seven eligible for child benefit:

On earnings between £12,570 (the personal allowance) and £50,270 (the higher rate threshold), an employee faces an effective tax rate of 28% – 20% basic rate income tax and 8% Class 1 National Insurance contributions (NICs – which are income tax in all but name).

Between £50,270 and £60,000 (the high income child benefit taper threshold), their marginal tax rate is 42% – 40% higher rate tax and 2% Class 1 NICs.

From £60,000 to £80,000 (the top of the high income child benefit taper threshold), their marginal tax rate jumps to 53.7% – 40% basic rate tax, 2% Class 1 NICs and an 11.7% high income child benefit charge.

Between £80,000 and £100,000 (the personal allowance taper threshold), the marginal rate drops back to 42%.

Between £100,000 to £125,140 (the top of the personal allowance taper threshold), the marginal rate leaps 62% – 40% higher rate tax, plus another 20% income tax as the personal allowance is tapered away and 2% Class 1 NICs.

Beyond £125,140 (the additional rate threshold) the marginal rate drops again to 47% – 45% additional rate tax and 2% Class 1 NICs.

There are two other complexities worth noting, which we have avoided to keep the graph simple:

In Scotland there are six income tax rates, creating further distortions and a marginal rate in the £100,000-£125,140 band of 69.5% - 45% advanced rate tax, plus another 22.5% income tax as the personal allowance is tapered away and 2% Class 1 NICs.

At £100,000 there is a cliff edge where tax-free childcare and, outside Scotland, some or all free childcare, is lost. The marginal tax rate in those circumstances heads towards infinity – an extra £1 of income can mean the loss of thousands of pounds in benefits.

Will the government do anything?

The concerns of the OBR and OECD echo criticisms which have been around for many years from think tanks such as the Institute for Fiscal Studies. Unfortunately, Chancellors have little incentive to make the system more rational:

The data to understand the impact of the distortions does not exist. Last November, a Freedom of Information Request revealed the Treasury has no estimate for the income tax revenue lost because parents act to keep income below the £100,000 threshold.

To remove the kinks would cost billions which the Treasury does not have. Even if it did, there would probably be other more deserving candidates, such as defence.

Any attempt to make the system smoother without reducing revenue would inevitably create winners and losers. The former are generally silent, whereas the latter tend to be uncomfortably noisy.

The anomalies are poorly understood because of the complex way in which they operate, which suits politicians. Stealth taxes have never been high on the priority list for reform and Rachel Reeves has shown little interest in redesigning the tax system.

As with the frozen allowances, doing nothing benefits the Treasury. According to the latest HMRC projections, about £1 in every £8 of income tax comes from those taxpayers with income in the £100,000-£150,000 band, almost as much as paid by their higher earning counterparts in the £200,000-£500,000 band.

What can you do?

The starting point is to work out what your income is for 2026/27, so that you know where you fit on the roller coaster graph above. That is not quite as easy as it sounds because the definition of income is not straightforward – advice may be necessary. If your income is in the taper band for high income child benefit or personal allowance, think about whether you can bring the income down. There are a variety of options, including:

Reduce your working hours. This may sound counter-intuitive, but for some people, forsaking £20,000 of taxable income to gain childcare benefits can make financial sense.

Pension contributions. Paying into a pension reduces your ‘income’ when calculating how taper applies and entitlement to childcare. The popularity of this option was partly behind the Chancellor’s 2025 Budget measure to limit the use of salary sacrifice for pension contributions, albeit not until 2029/30.

Restructure your investments. The way in which investments are held can determine what – if any – income you receive from them for tax purposes. ISAs are the obvious example because their income is not subject to UK tax, but there are other options. For example, you could transfer investments to your spouse/civil partner – provided you do not create a threshold problem for them. (Any such transfer must be outright and unconditional.)

Action

Early in the tax year is the best time to start planning – before too much income accrues.

Even if the tax thresholds have not been a problem for you in the past, those constant freezes mean they might be in 2026/27.

This article was prepared by Chris Green, our Head of Financial Planning. We always appreciate your feedback. If you have enjoyed this article or have any specific topics you would like to see addressed in future newsletters, please email us at FPTeam@city-asset.co.uk.