ICARA Disclosure

2026

1. Overview

In January 2022 the FCA introduced the Investment Firms Prudential Regime (IFPR), a new regime for UK firms authorised under the Markets in Financial Instruments Directive (MiFID). The regulation that formalises this regime is called MIFIDPRU. Under IFPR, firms’ own assessments are carried out under the ICARA process (Internal Capital Adequacy and Risk Assessment). The newregime is better suited for the investment management industry. It departs from the banking-based regulation of CRD/CRR which required the execution of an ICAAP (Internal Capital Adequacy and Assessment Process). In comparison to ICAAP, the ICARA has different start and end points. Risk analysis, under ICARA starts by analysing the firm’s business model and therefore it introducesactivity-based capital requirements for the firm. The ICARA process is an assessment of own funds and liquidity requirements given a firm’s business model and risk appetite.

1.1. Objective

This disclosure statement (the 'Statement') has been prepared by City Asset Management plc ('CAM', also referred to as the 'Company' or the 'Firm') in order to fulfil the regulatory disclosure requirements set out by the Financial Conduct Authority ('FCA') in the Prudential sourcebook for MiFID Investment Firms ('MIFIDPRU') Chapter 8.

CAM’s ICARA will be updated and approved by the Board annually or upon material change and is therefore an ongoing process that the firm monitors.

2. Basis of Disclosure

This report is prepared for the financial year end September 2025.

2.1. Frequency of Disclosure

Unless otherwise stated, all figures are as at 30 September 2025, the Company's financial year end, in accordance with the rules set out in chapter 8 of MIFIDPRU. MIFIDPRU 8 disclosures are published annually and concurrently with the Annual Report and Accounts in accordance with regulatory guidelines.

2.2. Location

MIFIDPRU 8 disclosure report is available on the Firm's website at: https://www.city-asset.co.uk/ICARA-disclosure.

3. Corporate Background

Founded in 1988, we have always prided ourselves on being able to offer a personalised and holistic service to our clients on an intergenerational basis. Historically, CAM has benefitted from both a strong, simple corporate structure and healthy balance sheet, which have allowed us the flexibility to manage steady growth. We do not have to chase short term opportunities to increase cash flow, only to suffer the spiralling costs associated with expanding the business in an erratic manner. Instead, we can take a more strategic and longer-term view, examining areas of opportunity whilst maintaining our focus upon and the quality of our core offering and strengths.

4. Company Activities

There are three main business areas for the Company:

Discretionary Asset Management for Direct Clients.

Financial Planning for Direct Clients.

Discretionary Asset Management for IFA introduced Clients.

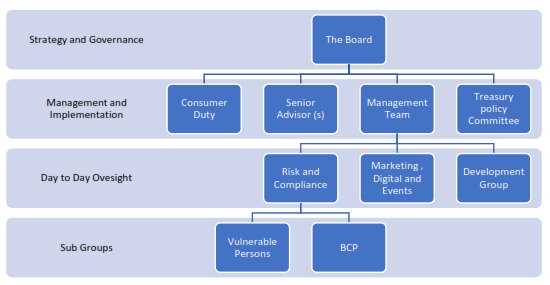

5. Risk Management objectives and policies

The Risk and Compliance Committee ‘RACC’ provides support between the Executive Committee ‘EXCO’, the Board and day to day management. It provides the facility to discuss risk and compliance issues at a granular level. Any important issues will be fed to the EXCO, and several Board members sit on the RACC. All RACC minutes are provided to all EXCO members from the monthly RACC meetings. The RACC is attended by representatives of all the departments within the business.

The Risk Management Framework is the structure and governance applied in the management of risks. This can be detailed through our governance structure and is included within our handbooks.

The Board, Executive Committee and the RACC review relevant management information in light of new risks, change assessment of risk and other issues through the monthly MI review. Decisions are taken as to whether risks are above or within CAM’s risk appetite. If it is established that a risk is outside CAM’s risk appetite, Senior Staff will take action to strengthen controls or the Board will revisit the Firm’s risk appetite.

5.1. Organisational Structure

The Board has delegated the day-to-day running of the business to the Executive Committee to review the strategic plan and look at the MI of the business. The Board meets Bi-monthly on strategic and governance matters with representatives from the Executive Management team reporting into the Board. The Executive Management team comprises individuals from all areas of the business. The organisational structure helps CAM oversee its risks and is an integral part in terms of identifying, mitigating and contributing to our risk management oversight in the business.

The Risk and Compliance Director has day-to-day responsibility for the effective operations of CAM’s Risk Management Policy, with oversight provided by the Board. The Risk and Compliance Director reports directly to the CEO and is a member of the Board.

5.2. Board

| Senior Management Function |

Name |

Outside Directorships in scope of MIFIDPRU 8.3.1 |

|---|---|---|

| SMF1 Chief Executive SMF 3 Executive Director SMF9 Chair of Governing Body |

Nicholas Coghill |

0 |

| SMF3 Executive Director |

Mark Rushton |

0 |

| SMF3 Executive Director SMF16 Compliance Oversight SMF17 Money Laundering Reporting Officer |

Rebecca Fifield |

0 |

| SMF3 Executive Director |

Chris Green |

0 |

| SMF3 Executive Director |

David Willcox |

0 |

| NED |

Kate Turner |

0 |

5.3. Approach to Diversity

Diversity is an opportunity for clients, employees and the firm to value different perspectives so that we can better serve our clients and employees. A corporate culture where everyone feels they belong is important to our goals. CAM values the creativity that diversity of thought brings and understand it plays a crucial role in strong governance and culture. Our focus on diversity spans across all aspects of the business from new talent, continued education, and recognition that a content and varied workforce is one of our greatest strengths.

CAM values and actively strives to have a diverse and inclusive workforce in a working environment free from discrimination. An inclusive work culture where people of different backgrounds are valued equally will ensure better outcomes for us all. We continually engage with our staff as well as external partners to help us to understand how we can make our workplace more inclusive and gain an insight into what our staff need most from us.

The Company will seek to promote the principles of equality, diversity and inclusion in all its dealings with employees, workers, job applicants, clients, customers, suppliers, contractors, recruitment agencies and the public.

5.4. Risk Management Overview

At a high level, CAM has defined its risk appetite to represent the amount and type of risk it is prepared to seek, accept or tolerate in the course of achieving its strategic objectives. The Company has not tended to have any great level of tolerance for risk and has always functioned with a strong Balance Sheet and capital position. At a lower level, balanced mixes of qualitative and quantitative measures are employed together with more granular tolerances and thresholds, where appropriate, to assess individual risks against CAM’s risk appetite and these are fully detailed in the Risk Register.

CAM has a low tolerance where risks are born of regulatory requirements and affect reputation. However, the Board recognises that, due to the industry and the nature of business, there may be areas where we tolerate a higher level of risk to facilitate core business processes while not creating unnecessary burdens.

The primary risk that CAM faces is created by market exposure and therefore, by definition, fluctuations in the value of assets under management and advice as a result of investment performance risk. CAM has always adopted a cautious approach with regard to the investment of client funds. It is the Directors’ view that in a majority of our multi-asset services, a real return on investments in excess of risk-free benchmarks is a preferable target to achieving riskier short-term gains, the fundamental objective being the preservation of clients’ capital. This strategy looks to provide steady organic growth which is sustainable in the long term.

CAM’s approach to the holistic risk framework is evidenced through a number of processes, which have provided a solid structure in previous years. The risk management framework embodies the policies, procedures and systems that CAM has implemented to identify, manage and mitigate its risks.

With the overall low risk appetite in mind, CAM has designed an appropriate control environment. This incorporates senior management arrangements, organisational structures, combined assurance framework, senior management reporting and monitoring systems, together with the necessary financial, operational, HR and IT/Project policies, procedures and systems. The resulting framework is reviewed regularly by the RACC, a subcommittee of the Executive Committee, and by the Board, to ensure it is appropriate in the context of the Group’s material risk and stated risk appetite.

CAM adopts a ‘top down’ and ‘bottom up’ approach to the identification of risks. CAM has identified the risks that could impact the ability of the business to meet its strategic objectives and these are reviewed against our risk appetite on an ongoing basis. Risks can be further identified through CAM’s incident reporting programme.

As part of our Risk Framework, CAM maintains a Risk Register. The Register is open to contribution from all staff and departments are expected to contribute to the understanding of risks for CAM as a whole.

The Risk Register is maintained and monitored by the Risk and Compliance Director. The RACC regularly reviews the register to ensure that it remains current and that the risk environment is clearly understood. Updates may be made as a result of discussion at RACC or Board level or in response to an Incident Report that highlights a particular issue.

The risks are largely focused on the day-to-day departmental operations, procedures and any potential impact on consumer outcomes and to avoid potential harm to customers.

The purpose of the Risk Register is to consistently facilitate:

Identifying and assessing new and existing risks at a granular level.

A methodology for considering individual impacts, probabilities, gross risk, control strengths and resulting net risks on a relative and qualitative basis.

A review tool to assess the impact of risks.

A means of prioritising risk-related actions (e.g., strengthening controls).

A means for reviewing the understanding of identified risks and assessing the implication of any amendments to net risk scoring and consequential impacts on risk tolerance, risk appetite and capital allocations.

The Risk Register now looks at firm, market or client harm as an output.

The Risk Register, therefore, provides a link between the bottom-up granular approach, or day to day risk management, and the top-down settling of risk appetite, identification of the high impact top-level risks and individual risk tolerances. All these items aid the Board in its assurance on the completeness of the IFPR requirements.

5.4.1 Material Risks

The firm is exposed to existing and emerging risks and vulnerabilities from changes in operational and economic circumstances. Given the nature of its business and operating model, the firm’s risk and compliance committee and senior personnel have decided that the following material risks have the potential to cause severe but plausible harms to the clients and the firm.

| Risk | Definition | Key Risks identified |

|---|---|---|

| Conduct Risk | Harm to clients as a result of inappropriate behaviour by CAMs business | SMCR Breaches Inconsistent Consumer outcomes |

| Counterparty / Credit | 3P Failure causes client loss | Wrapper / platform failure Bank default on client cash |

| Distribution | Incorrect or targeted marketing | Financial promotions Marketing strategy not followed |

| Economic | Economic environment impacts people and financial wellbeing | Virus strains War Cost of living |

| Investment Performance | Portfolios do not perform in line with Client expectations | Alignment Illiquid portfolio Investment Process and research |

| Legal and Regulatory | Exposure to legal and regulatory penalties, client loss and potential firm failure but not following applicable rules and laws | Data Breaches CASS Complaints Tax Reporting Suitability and record keeping failings Legacy back book PI cover Trusts Vulnerable Clients ESG SYSC failures Consumer Duty |

| Liquidity | Inability to meet expenses as they fall due | Unbudgeted items Corporate cash unavailable |

| Operational | Inadequate or failed internal processes, people, systems or from external events or partners. | Poor accounting ledgers Transfers Tax investing Inflation Systems Cybercrime Custodian failures Cybercrime |

| People | Employees fail to act in line with the firm’s expectations | Crime / Fraud Training |

| Political | Changes in legislation impacting the way we do business | Policy and Documentation changes |

| Technical | Business interruption through technological issues | Data security compromise Software and hardware failure |

All risks are assessed on a probability basis together with an impact assessment. The control mechanisms and current risk mitigation strategies in place against each risk are assessed by the managers responsible for each functional risk area. Senior Staff and the Board are responsible for challenging such assessment, with Risk and Compliance providing further challenge. In addition, the strength of controls is considered by the Risk and Compliance team as part of compliance monitoring and reviews. Together, any action recommended to improve those controls to ensure the risk is contained or is brought back within appetite is taken when required. The preventative and detective control aspects for each risk are assessed separately to give an overall control strength rating.

6. Own Funds Threshold Requirement

Under MIFIDPRU, CAM is required to disclose:

A reconciliation of common equity tier 1 items, additional tier 1 items, tier 2 items, and the applicable filters and deductions applied in order to calculate the Own Funds of the firm – see Table 1 below;

A reconciliation of 1 (above) with the capital in the balance sheet in the audited financial statements of the firm – see Table 2; and

A description of the main features of the common equity tier 1 instruments, additional tier 1 instruments and tier 2 instruments issued by the firm – see Table 3.

Table 1 – Composition of regulatory own funds (30 September 2025)

| |

Item |

Amount (GBP) |

Source based on reference numbers / letter of the statement of financial position in the audited financial statements |

|---|---|---|---|

| 1 |

Own funds |

7,106,962 |

n/a – sum of items below |

| 2 |

Tier 1 capital |

7,106,962 |

|

| 3 |

Common Equity Tier 1 capital |

6,350,522 |

|

| 4 |

Fully paid up capital instruments |

0 |

|

| 5 |

Share premium |

0 |

|

| 6 |

Retained earnings |

6,127,378 |

|

| 7 |

Accumulated other comprehensive income |

0 |

|

| 8 |

Other reserves |

235,296 |

|

| 9 |

Adjustments to CET1 due to prudential filters |

0 |

|

| 10 |

Other funds |

0 |

|

| 11 |

Total deductions from common equity Tier 1 |

-12,152 |

|

| 19 |

CET1: Other capital elements, deductions and adjustments |

0 |

|

| 20 |

Additional Tier 1 capital |

756,441 |

|

| 21 |

Fully paid up capital instruments |

82,190 |

|

| 22 |

Share premium |

674,250 |

|

| 23 |

Total deductions from additional Tier 1 |

0 |

|

| 24 |

Additional Tier 1: Other capital elements, deductions and adjustments |

0 |

|

| 25 |

Tier 2 Capital |

0 |

|

| 26 |

Fully paid up capital instruments |

0 |

|

| 27 |

Share premium |

0 |

|

| 28 |

Total deductions from Tier 2 |

0 |

|

| 29 |

Tier 2: Other capital elements, deductions and adjustments |

0 |

|

Table 2 - Own Funds: reconciliation of regulatory Own Funds to balance sheet in the audited financial statements (30 September 2025)

| |

|

Statement of financial position as in published / audited financial statements (as at period end) |

Under regulatory scope of consolidation (as at period end) |

Cross reference to template OF1 (above) |

|---|---|---|---|---|

| Assets – Breakdown by asset classes according to the statement of financial position in the audited financial statements |

||||

| 1 |

Property, plant and equipment |

51,694 |

n/a |

n/a |

| 2 |

Right of use assets |

0 |

n/a |

n/a |

| 3 |

Intangible assets |

12,152 |

n/a |

n/a |

| 4 |

Investment in subsidiary |

0 |

n/a |

n/a |

| 5 |

Loans to affiliate |

0 |

n/a |

n/a |

| 6 |

Other non-current assets |

0 |

n/a |

n/a |

| 7 |

Trade and other receivables |

2,394,709 |

n/a |

n/a |

| 8 |

Current tax asset |

0 |

n/a |

n/a |

| 9 |

Cash and cash equivalents |

6,117,381 |

n/a |

n/a |

| |

Total Assets |

8,575,936 |

|

|

| Liabilities – Breakdown by liability classes according to the statement of financial position in the audited financial statements |

||||

| 1 |

Lease liabilities |

0 |

n/a |

n/a |

| 2 |

Deferred tax liability |

0 |

n/a |

n/a |

| 3 |

Other non-current payables |

0 |

n/a |

n/a |

| 4 |

Trade and other payables |

1,456,821 |

n/a |

n/a |

| 5 |

Lease liabilities |

0 |

n/a |

n/a |

| |

Total Liabilities |

1,456,821 |

|

|

| Shareholders’ Equity |

||||

| 1 |

Share capital |

82,190 |

n/a |

Item 4 |

| 2 |

Share based payment reserve |

159,854 |

n/a |

|

| 3 |

Retained earnings |

6,877,071 |

n/a |

|

| |

Total Shareholders’ Equity |

7,119,115 |

|

|

Table 3 - Own funds: main features of own instruments issued by CAM (30 September 2025)

CAM does not have any other capital instruments aside from share capital in issuance.

6.1 Own Funds regulatory requirement

The level of regulatory capital that must be held to absorb losses is the Own Funds Threshold requirements. This report has been based on the fact that CAM is an SNI firm for the purposes of IFPR and ICARA. CAM received FCA approval to relinquish CASS permissions (Jan 2024) following receipt of Auditor’s 30 September 2023 limited assurance report.

Given that CAM is an SNI investment firm, the own funds requirements is the higher of the following two items:

6.2 Permanent Minimum Capital Requirement

The PMR is the minimum level of own funds that an investment firm must always hold based on the MiFID activities it has permission to undertake. The three levels of PMR are £750,000, £150,000, and £75,000. These replace the fixed capital thresholds quoted in Euros in CRD IV.

Under MIFIDPRU 4.4.4R, CAM fulfils the conditions, so our PMR is £75k as at 30 September 2025.

6.3 Fixed Overhead Requirement

MIFIDPRU 4.5 sets out the FOR an investment firm. This represents one quarter of the relevant expenditure in the previous financial year.

This is £1,773,000 based on the financial year ended September 2025.

6.4 Meeting the Overall financial adequacy rule

CAM must ensure, that at all times, its Own Funds and liquid assets are held throughout an economic cycle to remain financially viable and address potential material harm from its ongoing activities. This is supplemented by adequate resources to enable an orderly wind down.

CAM has a Treasury committee in place that reports to the Board and is responsible for monitoring this requirement. This will be a dynamic process as risks materialise over the course of the year. CAM operates with a significant regulatory and liquidity buffer and

The firm’s threshold requirement is the higher of its Permanent Minimum Requirement (PMR), and Fixed OverheadRequirement (FOR).

The firm’s overall PMR and FOR requirement have been assessed to be £75,000 and £1,773,000, respectively.

The Fixed Overhead Requirement (FOR) is based on the firm’s quarter of expenses. The firm has assessed that its wind down costs would be substantially more than its FOR, The Threshold requirement for the firm is the higher of PMR, KFR and FOR. On this basis the Threshold Requirement for the firm is £1,773,000 although we have decided to opt for the wind down £2,000,000 from a prudence perspective.

The early warning indicator has been set 110% of the Threshold Requirement. The following table provides an overview.

Own Funds Threshold requirement and EWI

| Category |

Capital Requirement (£) |

|---|---|

| Own Funds |

£7,106,962 |

| PMR |

£75,000 |

| FOR |

£1,773,000 |

| Additional budgeting for wind-down excess costs |

£227,000 |

| Threshold Requirement |

£2,000,000 |

| Early Warning Indicator |

£2,200,000 |

| Surplus to EWI |

£4,906,962 |

| Wind-down Trigger |

£1,773,000 |

Note: the winddown trigger is assumed to be 100% of the firm’s FOR as per guidance. Note that this is below the threshold requirement given the additional capital budgeting that has occurred.

The ICARA process is central to a firm’s risk management framework under the regulatory regime. It is not only integral to how the firm manages risk but is also central to how the FCA manages the risk of the firm that it supervises.

As part of the ICARA process the Board and governing committees oversee and assess:

Identification and monitoring of risks or harms;

Details of any financial and non-financial mitigations implemented;

Forecast capital and liquidity needs on an ongoing basis and in the event that the firm may have to wind-down;

Determine appropriate and credible recovery actions to prevent breaching a threshold requirement;

Undertake wind-down planning; and

Assess the adequacy of the firm’s own funds and its liquidity requirements.

6.5. Own Liquidity Threshold Assessment

The firm’s basic liquidity requirement is set by the regulator to be 33.3% of its FOR. Since FOR is 25% of the firm’s annual expenses, the basic liquidity requirement equates to 1 month of expenditure.

The own liquidity threshold requirement (OLTR), however, needs to take account of unexpected payments and obligations and factor in wind down costs or other risks that have not been accounted in the capital budgeting process. As the firm’s Own Funds Threshold Requirement is derived from its FOR (rather than PMR), it is appropriate to calculate the OLTR on a similar basis (as utilisation of the monthly derivation of the own funds calculation would produce a figure significantly less than the basic liquidity requirement).

The firm is required to calculate the maximum amount of liquid assets required to operate the business for one quarter (considering the wind down scenarios previously noted).

Basic liquidity Requirement: £591,000

Own Liquidity Threshold Requirement: £2,000,000*

EWI (110% OLTR): £2,200,000*

In calculating its OLTR the firm has considered its position with respect to FOR and wind down assumptions. From a prudence perspective the firm has decided to use the wind down assumptions as its OLTR.

The firm meets its OLTR through a combination of cash and deposits on its balance sheet together with investment in corporate and government backed debt securities. As of the 30th September 2025, the firm held £6.1m in liquid assets and cash on its balance sheet.

The combination of Core liquid assets with current Gilt investments means that the Board are comfortable that the firms current liquidity profile and financial strength give no concern that the OLTR or EWI is near breach. The stress testing model also indicates that there will no danger of breaches even in the event of a significant market downturn. In the unlikely event that a material downturn occurs per the stress testing, CAM would convert liquid assets such as corporate and government debt into cash.

6.6. Assessment Process

The ICARA sets out the firm’s assessment of its risks and harms post mitigation and whether further capital is required in addition to the requirements set out by the FCA, specifically FOR. Any additional own funds are to be recorded and agreed within the ICARA process. Scenario analysis is to be conducted and documented within the ICARA to assess the potential financial impact of specific events on the firm and whether the firm would remain a going concern.

The firm is required to provide information from the ICARA to the FCA on a periodic basis via a number of regulatory returns. The FCA has also implemented an annual ICARA questionnaire (regulatory return MIF007).

The outcome of the ICARA is formally approved by the Board at least annually, with more frequent reviews if there is a fundamental change to the business or the operating environment.

7. Remuneration policy

CAM meets the conditions in MIFIDPRU 7.1.4R(1) for reduced disclosure requirements on the basis that the value of the firm’s on- and off-balance sheet items over the preceding 4-year period taken as a rolling average is below £300million and CAM has no trading book assets.

7.1 Remuneration Committee

CAM does not operate a standalone Remuneration Committee given its size. The Board oversees all remuneration, with specific approval from the NED, and will seek input from HR, senior management and/or the control functions, as appropriate.

7.2 Remuneration Overview

The link between pay and performance Compensation payments is made up of a mixture of fixed salary paid monthly and a discretionary variable bonus, which is paid in cash after the financial year-end and following individual performance appraisals. Total compensation includes a range of benefits associated with employment including, but not limited to, private health insurance, pension contributions and death in service insurance.

Remuneration is designed to reward performance, with the overall package intended to generally reflect market practice for any given role. The Company’s remuneration structure comprises a fixed salary element, which is intended to reflect an employee's professional experience, high standard of regulatory behaviour and organisational responsibilities and is distinct from variable remuneration which is intended to reward performance in excess of that required to fulfil the employee's job description.

Discretionary variable bonuses are paid following a 12-month performance review of the financial period to which they relate. All variable pay awards are conditional, discretionary and contingent on sustainable delivery of activities under individual job descriptions, high standards of expected corporate behaviours, exemplary regulatory performance and risk adjusted performance. Share options are also awarded on a discretionary basis to staff as a mean of aligning long term strategic participation and involvement with the business.

Sales Team members are remunerated on a basis of the type and amount of new funds introduced to the business from the IFA community. This is paid on a monthly basis.